Student Loan Forgiveness for Teachers: What Actually Works

Most teachers find out about loan forgiveness the wrong way: a vague mention from HR during onboarding, a Facebook post from a colleague, or a panicked Google search in year four. Here's what rarely gets said upfront — there are three separate federal programs that can eliminate your student debt, and picking the wrong one, or combining them in the wrong order, can cost you five extra years of payments. The math matters more than the marketing.

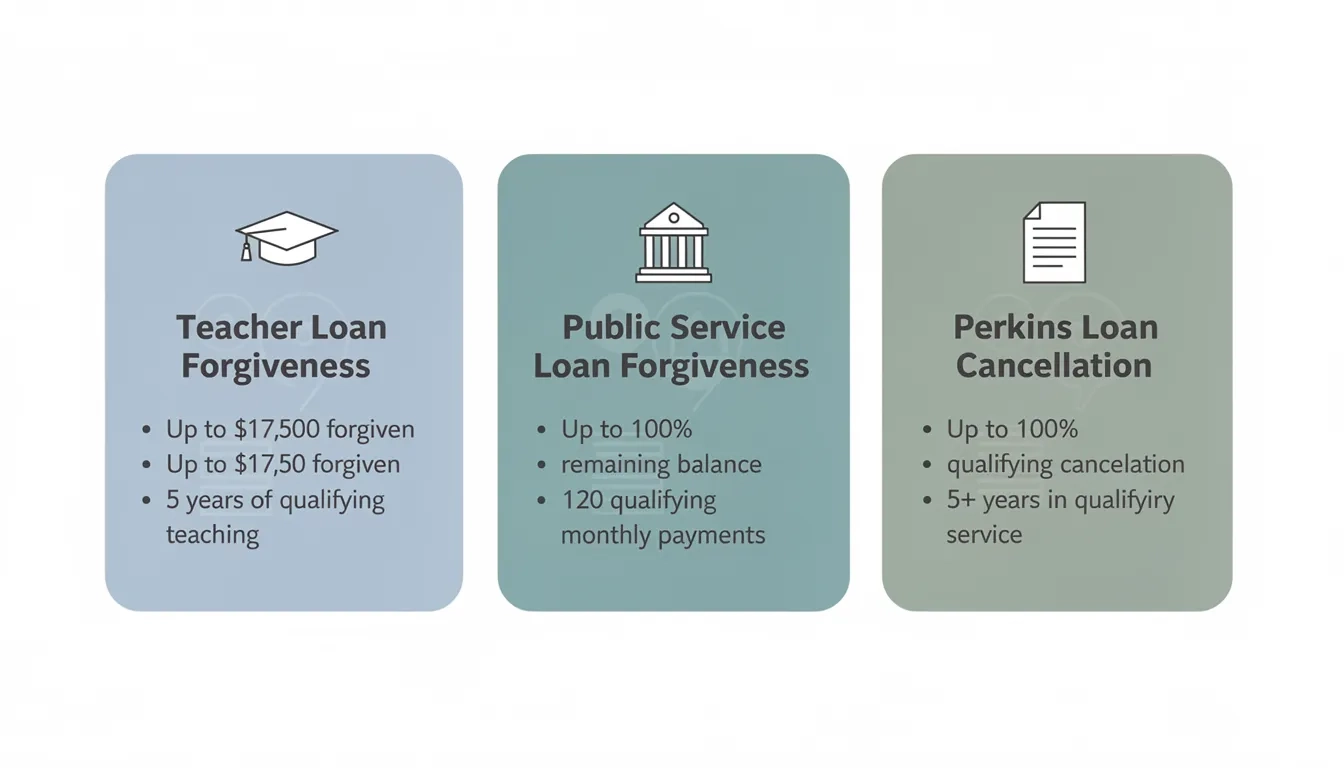

The Programs at a Glance

Three federal programs cover most teachers. They work differently, forgive different amounts, and target different borrower profiles.

- Teacher Loan Forgiveness (TLF): Up to $17,500 erased after five consecutive years at a qualifying low-income school. Fast, but capped.

- Public Service Loan Forgiveness (PSLF): Your entire remaining balance forgiven after 120 qualifying monthly payments. No cap, but requires ten years.

- Perkins Loan Cancellation: Up to 100% of your Perkins loans wiped out over five years of qualifying service. Only applies if you have older Perkins debt — the program stopped issuing new loans in 2017.

All three are permanently tax-free at the federal level. That distinction carries more weight now than it did two years ago, for reasons we'll get to.

Teacher Loan Forgiveness: The Program Most Teachers Misread

TLF sounds like a universal win. For most teachers, it isn't.

The $5,000 vs. $17,500 split is the first thing to understand. Most qualifying teachers — elementary generalists, English teachers, social studies teachers — receive $5,000. The full $17,500 is reserved for two specific categories: highly qualified secondary teachers of mathematics or science, and special education teachers at any grade level. If you teach fourth grade reading, you're not getting $17,500.

To qualify for TLF, you need all of this:

- Five complete and consecutive academic years at an eligible low-income school or educational service agency

- Direct Loans or FFEL Stafford Loans taken out before the end of your five qualifying years

- "Highly qualified" teacher status as defined under federal education law

- No outstanding balance on a Direct Loan or FFEL as of October 1, 1998

The word "consecutive" is strict. A gap year, an unapproved leave of absence, or a year teaching at a non-qualifying school resets the clock to zero.

Finding qualifying schools is more straightforward than it used to be. The Department of Education maintains the Teacher Cancellation Low Income Directory (TCLI), updated annually, listing every eligible Title I school. A school qualifies when it's in a district with a high proportion of low-income families — generally more than 30% of enrolled students from low-income households. Check the TCLI before accepting a position, not two years in.

A common misconception: teachers often assume any public school automatically qualifies. It doesn't. Your school must appear in the TCLI specifically, or be part of an educational service agency that qualifies. The list changes every year.

After completing five years, you apply through your loan servicer (MOHELA, Aidvantage, EdFinancial, etc.). Processing typically takes 60–90 days.

PSLF: The Unlimited Forgiveness Option

PSLF doesn't care how much you owe. That is the entire point.

After 120 qualifying monthly payments — ten years — whatever remains on your federal Direct Loans gets forgiven. If you borrowed $80,000 and paid down $30,000 through an income-driven repayment plan, the remaining $50,000 disappears. No ceiling. Tax-free.

For most teachers, PSLF is the more powerful program, especially for anyone who graduated with a master's degree (a requirement in many states, which means a meaningfully larger debt load) or who attended a private university. The Consumer Financial Protection Bureau, after reviewing teacher debt scenarios, identifies PSLF as "often the best option" for teachers with federal student loans. Student Loan Planner's case studies found that a teacher carrying a moderate balance saved close to $25,000 in total payments by choosing PSLF over TLF.

Public school teachers qualify on the employer side almost automatically — government organizations at any level are qualifying employers, and so are 501(c)(3) nonprofits. To make PSLF work, you need to:

- Hold eligible Direct Loans (FFEL or Perkins loans must be consolidated first)

- Enroll in a qualifying income-driven repayment (IDR) plan

- Work full-time for a qualifying employer — generally 30+ hours per week

- Submit an Employment Certification Form every year to document progress

The IDR enrollment piece is not optional if you want PSLF to pay off. Making standard 10-year repayment payments means you pay off the loan entirely before reaching 120 payments. Lower monthly IDR payments keep a balance alive to be forgiven at year ten, which is where the actual savings accumulate.

TLF vs. PSLF: The Decision That Could Cost You Years

You can use both TLF and PSLF in the same teaching career. But the same five years cannot count toward both. The years you use to qualify for TLF don't count toward PSLF's 120-payment requirement.

Pursuing TLF first, then PSLF, extends your total forgiveness timeline to 15 years. That's five years for TLF, then another ten for PSLF's 120 payments. For a teacher with $70,000 in debt, you'd collect $5,000–$17,500 up front and then wait a decade more. Compare that to ten years straight under PSLF with your entire remaining balance forgiven at the end.

| Strategy | Loan Balance | Years to Forgiveness | Outcome |

|---|---|---|---|

| PSLF only, starting year 1 | $70,000 | 10 | Remaining balance (~$50K+) forgiven |

| TLF ($17,500) first, then PSLF | $70,000 | 15 | Both amounts forgiven, but 5 years longer |

| TLF ($17,500) only | $22,000 | 5 | $17,500 forgiven — nearly 80% of balance |

| TLF ($5,000) only | $70,000 | 5 | Just $5,000; large balance remains |

The math flips for teachers with smaller balances. If you graduated with $22,000 in loans — common for teachers who attended in-state public universities — TLF can erase $17,500 of that in five years, clearing nearly 80% of the debt. That beats waiting ten years for PSLF to forgive a comparatively small remaining balance.

A practical decision framework:

- Debt under $30,000 → Run TLF numbers; it may clear most of your balance faster

- Debt between $30,000 and $50,000 → PSLF is often better unless your subject qualifies for the $17,500 tier

- Debt over $50,000 → PSLF only, start tracking from your first paycheck

One action most borrowers miss: FFEL loans don't qualify for PSLF. If you have older federal loans, you need to consolidate them into a Direct Consolidation Loan before any payments start counting. Teachers have lost years of qualifying credit by discovering this in year eight.

Perkins Loans and State Programs: The Overlooked Extras

Perkins Loan cancellation runs on its own separate track. If you carry older Perkins debt, you can eliminate up to 100% over five years of qualifying service. The cancellation schedule is specific: 15% in year one, another 15% in year two, 20% in year three, 20% in year four, and 30% in year five. Interest that accrues during qualifying service periods is also canceled. You apply through the institution that originally issued the Perkins loan — not a federal servicer.

Beyond federal programs, state repayment assistance is worth 20 minutes of your time. The devil is in the details — most programs have subject-area requirements, income limits, or school-type restrictions — but stacking a state award on top of a federal one is allowed, and they don't interfere with each other.

A few examples from around the country:

- Texas offers up to $2,500 per year through the Teach for Texas Loan Repayment Assistance Program for teachers in shortage subject areas at public schools

- Colorado provides up to $5,000 per year through its Educator Loan Forgiveness program, targeted at rural and underserved schools

- Arkansas offers up to $6,000 in total repayment assistance for qualifying teachers

- Minnesota maintains at least 21 distinct loan forgiveness or reimbursement plans for educators across different subjects and regions

Get the Facts Out (getthefactsout.org) maintains a clean state-by-state database — far easier to navigate than hunting through each state education agency's website individually.

What Changed in 2025–2026

A few significant developments this year affect teachers specifically, and one of them changes the calculus on forgiveness options.

The SAVE plan is in legal limbo. This was the most affordable income-driven repayment option — many borrowers got monthly payments reduced dramatically under it. Court challenges have it frozen. A replacement called the Repayment Assistance Plan (RAP) launches July 1, 2026, but it runs for 30 years instead of 20. If you were counting on SAVE to keep your PSLF payments low, check which IDR plan you're currently enrolled in and whether it still qualifies.

IDR forgiveness is now federally taxable. The American Rescue Plan Act's tax exemption expired December 31, 2025. Starting in 2026, a borrower who gets $50,000 forgiven after 20 years of income-based repayment owes roughly $11,000 in federal income taxes (at a 22% bracket). PSLF, Teacher Loan Forgiveness, and Perkins cancellation are explicitly exempt from this change. This is one more argument for teachers to target the tax-free programs rather than letting loans drift toward 20-year IDR forgiveness as a backup plan.

New PSLF employer restrictions take effect July 1, 2026. Organizations deemed to have a "substantial illegal purpose" will be disqualified. The Department of Education estimates fewer than ten employers annually will be affected — standard public school districts and nonprofit schools are almost certainly untouched. Past qualifying service already logged is unaffected regardless.

Parent PLUS loans issued on or after July 1, 2026 lose PSLF eligibility under the new rules. If you or your family have Parent PLUS loans, check the disbursement dates carefully before planning forgiveness.

Bottom Line

- Know your debt load before committing to a strategy. Teachers with under $30,000 may find TLF clears most of the balance in half the time PSLF takes. Teachers with $50,000 or more should model PSLF from day one and skip TLF entirely.

- Start PSLF certification immediately, not eventually. Submit an Employment Certification Form every year. Documentation errors — not ineligible employers — are the leading reason teachers get denied after a decade of payments.

- Consolidate FFEL and Perkins loans into Direct Loans now if you haven't already. Payments on unconsolidated FFEL loans don't count toward PSLF, and this is only fixable before you need those years to count.

- Verify your school's TCLI status before counting on TLF. A school can drop off the directory, and you want to know before it affects your qualifying-year count.

- State programs stack with federal ones. A Colorado teacher pursuing PSLF can simultaneously collect state educator loan forgiveness. They're designed to work together.

The single most important thing: don't wait until year four or five to research this. Teachers who plan from year one reach forgiveness in year ten. Those who figure it out in year six face compressed, higher-stakes choices with less runway.

Frequently Asked Questions

Can I use Teacher Loan Forgiveness and PSLF at the same time?

You can use both in the same career, but not for the same years of service. The five years you spend qualifying for TLF don't count toward PSLF's 120-payment requirement. Combining them sequentially extends your total forgiveness timeline to 15 years instead of 10 — which matters a lot for teachers with large balances.

What counts as a qualifying school for Teacher Loan Forgiveness?

Your school must appear in the federal Teacher Cancellation Low Income Directory (TCLI), available at studentaid.gov. Qualifying schools are generally Title I schools where more than 30% of students come from low-income families. The directory updates annually, so check it before starting a new teaching position — not after.

Do private school teachers qualify for loan forgiveness programs?

Private school teachers can qualify for TLF if their school is a nonprofit listed in the TCLI. For PSLF, private schools must be tax-exempt 501(c)(3) nonprofits. Teachers at for-profit private schools are ineligible for both federal programs, though they may have state options.

Does maternity leave or FMLA break my consecutive years for TLF?

Paid leave and leave taken under the Family and Medical Leave Act generally preserve your consecutive year count for TLF. Resigning and returning in a later year does reset the clock. Before taking any extended leave, get written confirmation from HR about how the leave is classified against your qualifying service record.

Is teacher loan forgiveness taxable income?

No. Teacher Loan Forgiveness, PSLF, and Perkins Loan Cancellation are all permanently tax-free under federal law. This is a meaningful distinction from income-driven repayment forgiveness, which became federally taxable starting in 2026. If you're ever told otherwise, check the IRS guidance directly — the tax-free status is written into the statute for these programs.

Can I qualify for TLF if I teach multiple subjects?

Yes. If you teach both math and English at the secondary level, you may qualify for $17,500 based on your math instruction, provided you meet the "highly qualified" standard for that subject. The higher tier applies when you meet the eligibility criteria in at least one qualifying subject — you don't need to teach it exclusively.

Sources

- Teacher Loan Forgiveness/Cancellation - Federal Student Aid

- 4 Loan Forgiveness Programs for Teachers - Federal Student Aid

- PSLF vs. Teacher Loan Forgiveness for Teachers - Student Loan Planner

- Best Student Loan Forgiveness Option for Teachers - CFPB

- Student Loan Forgiveness 2026 Updates - The Payoff Climb

- Can You Use Teacher Loan Forgiveness and Then PSLF? - PeopleJoy

- Teacher Loan Forgiveness & Grants by State - Get the Facts Out