How Part-Time Enrollment Affects Federal Financial Aid

Before 2024, if you took 8 credits instead of 12, your Pell Grant got slotted into a fixed "three-quarter-time" bucket. You got the same payment whether you took 8 credits or 10. Then the FAFSA Simplification Act rewrote the rules. Starting with the 2024-2025 award year, the Department of Education scrapped enrollment categories entirely and moved to a credit-by-credit calculation. Every single hour now counts, proportionally. That one quiet change rippled through the finances of millions of part-time students—most of whom have no idea it happened.

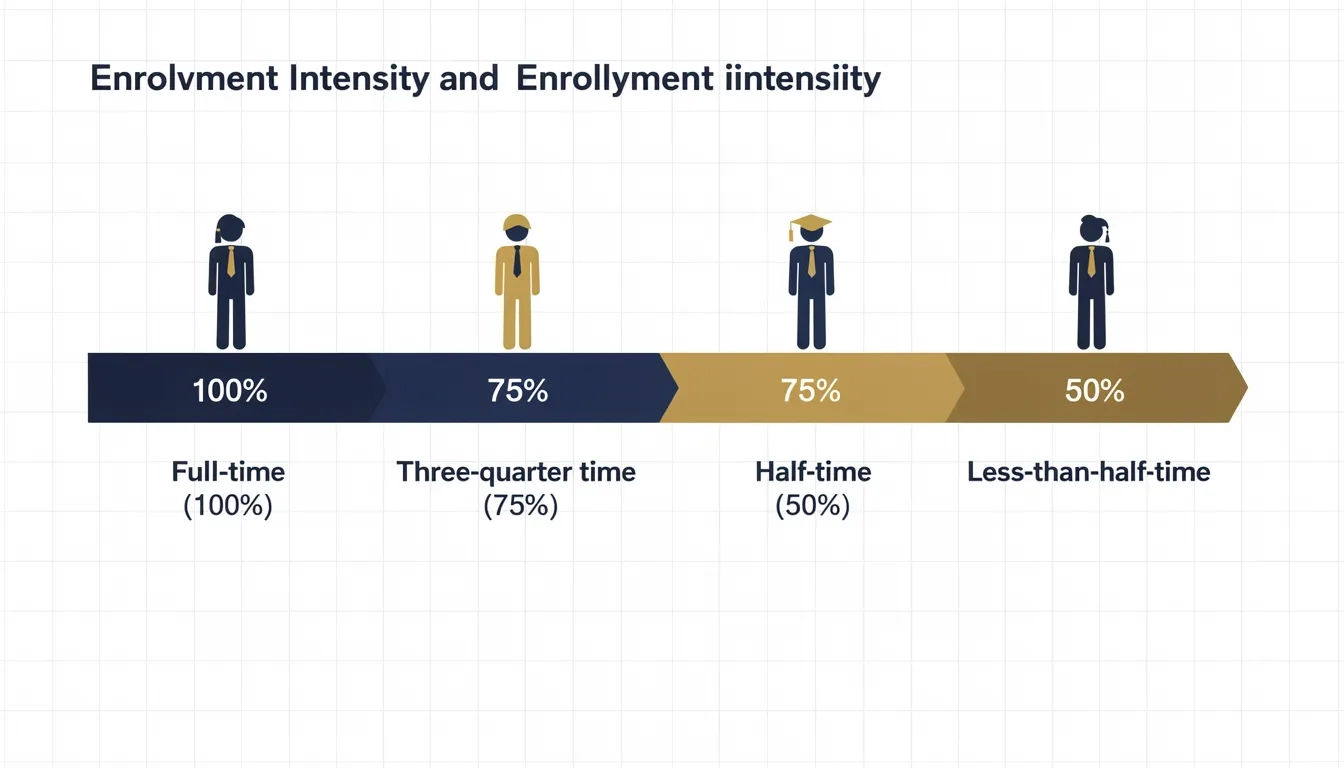

The Enrollment Intensity Model, Explained

The new system runs on something called enrollment intensity: the percentage of full-time enrollment you're actually taking.

The formula is simple. Divide your enrolled credits by what your school defines as full-time, then multiply by 100. If your school's full-time threshold is 12 credits and you're taking 9, your enrollment intensity is 75%. Take 6 credits and it's 50%. Take 3 and it's 25%. Your Pell Grant payment for that term gets scaled to match that percentage, dollar for dollar.

This replaced the old tiered system where students were bucketed as full-time, three-quarter-time, half-time, or less-than-half-time. Under the old buckets, the difference between 7 and 9 credits could cost you nothing. Under the new model, every credit hour has a price tag.

The shift from fixed enrollment tiers to continuous enrollment intensity is the most significant structural change to Pell Grant calculations in decades—and it rewards taking even one more class per semester.

How Pell Grants Get Reduced for Part-Time Students

Your scheduled Pell award is the anchor. It's the maximum you'd receive at full-time enrollment, calculated from your Student Aid Index (which replaced the old Expected Family Contribution). For 2024-2025, the maximum scheduled award is $7,395 and the minimum is $740—exactly 10% of the max, flagged by a specific code on your ISIR record.

Say your scheduled award comes in at $6,895 annually. Enroll at 75% intensity (9 of 12 credits) and your annual award becomes $5,171. Drop to 50% intensity (6 credits) and that figure falls to $3,447. At 25% intensity, you're looking at $1,723. The math is linear, not a cliff.

Here's the non-obvious part: you can receive a Pell Grant even enrolled in fewer than 6 credit hours. Less-than-half-time status doesn't shut off Pell. What it does change is how your Cost of Attendance gets calculated for aid purposes—only direct costs like tuition and fees count, not room and board or living expenses. So the effective reduction is bigger than the enrollment intensity alone suggests.

The FAFSA Simplification Act also removed the half-time enrollment requirement for Year-Round Pell. Students who take lighter summer loads can now access that third semester of Pell funding regardless of how many credits they're carrying—a real expansion that didn't get much press.

Federal Loans: The Half-Time Cliff

Pell Grants scale gracefully. Federal loans do not.

Direct Subsidized and Unsubsidized Loans require half-time enrollment, minimum. For most undergraduates that means 6 credit hours per term. Take 5 credits and you don't get a reduced loan. You get nothing—no federal borrowing that semester, period.

This creates a genuine trap. Many students go part-time precisely because they're managing jobs, childcare, or health issues—situations where they need financial support more than ever. The loan cutoff arrives right when things are hardest.

| Aid Type | Minimum Enrollment | What Happens Below That Threshold |

|---|---|---|

| Pell Grant | Any (even 1 credit) | Prorated by enrollment intensity |

| Direct Subsidized Loan | Half-time (≥6 credits) | No borrowing available that term |

| Direct Unsubsidized Loan | Half-time (≥6 credits) | No borrowing available that term |

| Federal Work-Study | Usually half-time | Varies by institution |

| SEOG Grant | Usually half-time | Varies by institution |

Subsidized loans also stop being subsidized the moment you drop below half-time. Interest starts accruing on your balance immediately—not after a grace period, not after you leave school. The day your school reports the enrollment change, the meter starts. You still have a six-month grace period before repayment kicks in, but the interest that builds during those six months gets added to your principal.

A student who drops from 6 to 5 credits mid-semester to relieve stress may not realize they just cost themselves months of compounding interest on balances they thought were still frozen.

What Happens When You Drop a Class Mid-Semester

Timing matters as much as the decision itself. Here's the sequence:

- Your school reports the enrollment change to the Department of Education, usually within 30 days.

- Aid already disbursed may require return if you drop before your school's census date—the date after which enrollment is "locked" for financial aid purposes.

- Loans enter their grace period the day your status drops below half-time.

- Your Cost of Attendance gets recalculated for the remaining portion of the term, often reducing your total aid package.

- Return of Title IV funds rules activate if you withdraw completely—you may owe back a prorated share of disbursed aid.

The census date is the line. Drop before it and your school typically recalculates aid from scratch for the whole term. Drop after it and you usually keep what was already paid out, though the next disbursement will reflect your new enrollment intensity. Either way, it's not a neutral decision.

Satisfactory Academic Progress: The Slow-Burn Risk

Most students know about grades and GPA. Fewer understand the SAP rules that can quietly eliminate all federal aid eligibility—and this is where part-time enrollment creates a particularly sneaky long-term problem.

Federal regulations require schools to evaluate Satisfactory Academic Progress across all enrollment periods, even semesters when you received no aid. A semester where you took 3 credits and withdrew from all of them still counts in your cumulative record.

Two specific rules bite part-time students hardest:

- The 67% completion rate standard. You must successfully complete at least 67% of all credit hours ever attempted. Fail or withdraw from too many individual courses over time and aid gets suspended—even if your GPA is fine.

- The 150% maximum timeframe rule. If your degree requires 120 credit hours, you can attempt up to 180 total before losing eligibility. A full-time student can absorb a few failed semesters and still finish within that window. A part-time student who also fails or withdraws from courses burns through their buffer much faster than they realize.

The National Association of Student Financial Aid Administrators (NASFAA) has specifically flagged that students who don't fully understand these cumulative rules often make enrollment decisions that feel reasonable semester-by-semester but erode their aid eligibility over time.

A Decision Framework Before Going Part-Time

Run through these before reducing your credit load:

- What's your current Pell scheduled award? Multiply it by your planned enrollment intensity to see your actual payment. If that number doesn't cover your tuition shortfall, you need a backup plan.

- Do you have existing subsidized loans? Going below half-time triggers interest accrual. Calculate the monthly cost. For a $15,000 subsidized balance at a 6.53% interest rate, you're looking at roughly $81 per month in new interest the day you drop.

- What's your cumulative completion rate? If you're already hovering near 70%, adding withdrawn credits pushes you into SAP warning territory.

- How close are you to the aggregate loan limit? Dependent undergraduates max out at $31,000 in total federal loans; independent undergraduates at $57,500. Going part-time doesn't extend those caps—you hit the ceiling at the same dollar amount, just spread over more time.

- Do you have state or institutional grants? Many state scholarships, unlike Pell, require full-time enrollment. Georgia's HOPE Scholarship, for example, requires 12 credits to receive maximum funding. Check those requirements separately—federal rules are the floor, not the ceiling.

Practical Things Part-Time Students Tend to Overlook

The timing of aid disbursement and enrollment verification creates a window where mismatches happen. Your FAFSA reflects your planned enrollment. Your school packages aid based on that plan. If you plan for 12 credits but actually register for 9, the school adjusts when it verifies your registration—usually within the first few weeks of the term.

Aid already disbursed typically isn't clawed back immediately. Instead, the school reduces the next disbursement. But students who already spent the full first disbursement expecting a full second one can get caught short.

One more thing that often gets missed: the Lifetime Eligibility Used counter ticks up even for reduced awards. Pell Grant eligibility is capped at 600% LEU, equivalent to about six full academic years. If you spend three semesters taking 6 credits each—receiving 50% of your scheduled award—you've used 150% of your LEU (three half-time semesters × 50%). You haven't stretched your Pell Grant eligibility by going part-time. You've spent real eligibility at a slower rate, but you're still spending it.

The writing's on the wall for anyone who assumes part-time enrollment is a way to make aid last longer. It reduces per-term payments, yes, but doesn't extend your lifetime eligibility proportionally unless you understand how LEU is calculated.

Bottom Line

Going part-time doesn't eliminate your federal aid—but it changes almost all of it, and not always in predictable ways.

- Pell Grants now scale credit-by-credit using enrollment intensity. Every hour you take fewer than full-time reduces your award proportionally. You can still receive Pell with just one enrolled credit, but the amount shrinks fast.

- Federal loans require at least half-time enrollment (typically 6 credits). Below that, no borrowing is available that semester. Subsidized loan interest also starts accruing the day you drop below half-time.

- SAP rules apply to every credit you ever attempt, regardless of aid status. Slow progress plus withdrawn courses is a fast path to losing eligibility under the 67% completion or 150% timeframe standards.

- State and institutional grants often have stricter minimums than federal programs—verify each one separately before dropping credits.

- Before changing your enrollment, talk to your financial aid office, check your SAP standing, and model the interest impact on any subsidized balances. Five minutes of math now can prevent a semester of financial scrambling later.

Frequently Asked Questions

Can part-time students qualify for any federal financial aid?

Yes. Part-time students can receive Pell Grants at any enrollment level, including fewer than 6 credit hours. Federal Direct Loans and most institutional grants require at least half-time enrollment (typically 6 credits). Federal Work-Study availability at less than half-time varies by institution.

Does dropping one class actually change my Pell Grant?

Starting with the 2024-2025 award year, yes. The FAFSA Simplification Act replaced fixed enrollment tiers with enrollment intensity—a percentage calculated credit-by-credit. Dropping from 12 to 11 credits reduces your Pell payment proportionally. Every credit hour now moves the number.

Is it a myth that you need full-time enrollment to get federal aid?

Yes, and it's one of the most persistent ones. You don't need to be enrolled full-time to receive Pell Grants or even to be eligible for federal loans. The real thresholds are: any enrollment for Pell, and half-time (6 credits) for federal loans. Students sometimes overload their schedules believing they'll lose all aid at anything below 12 credits—that's simply not how the system works.

What happens to my subsidized loans if I drop below half-time?

Interest starts accruing on subsidized loan balances the day your enrollment drops below half-time—not after your grace period begins. You have six months before repayment starts, but interest accumulates during those months and capitalizes onto your principal. If you re-enroll at half-time or more before the grace period ends, accrual stops.

How does part-time enrollment affect my Pell Grant lifetime eligibility?

Pell Grant eligibility is capped at 600% Lifetime Eligibility Used (LEU). Going part-time reduces each term's disbursement but still draws down your LEU at the rate of your enrollment intensity. Two semesters at 50% intensity use 100% of LEU—the same as one full-time semester. You're spending your lifetime eligibility more slowly in calendar time, but you're still spending it.

What should I do before officially switching to part-time?

Contact your financial aid office before registering for fewer credits, not after. Ask them to show you the exact aid recalculation, confirm your current SAP standing, and identify your school's enrollment census date. Making the change after the census date usually has less immediate impact on disbursed aid. Knowing that date can save you from a mid-semester financial surprise.

Sources

- Federal Pell Grant Program, 2024-2025 Federal Student Aid Handbook

- FAFSA Simplification Act Changes for Implementation in 2024-25

- Half-Time Enrollment – StudentAid.gov

- Can Part-Time Students Receive FAFSA? – Ascent Funding

- Explaining 2024-2025 Pell Grant Changes – McClintock CPA

- Enrollment Status for Federal Pell Grant – Mesa Community College