How Job Loss Affects Your FAFSA and Financial Aid Package

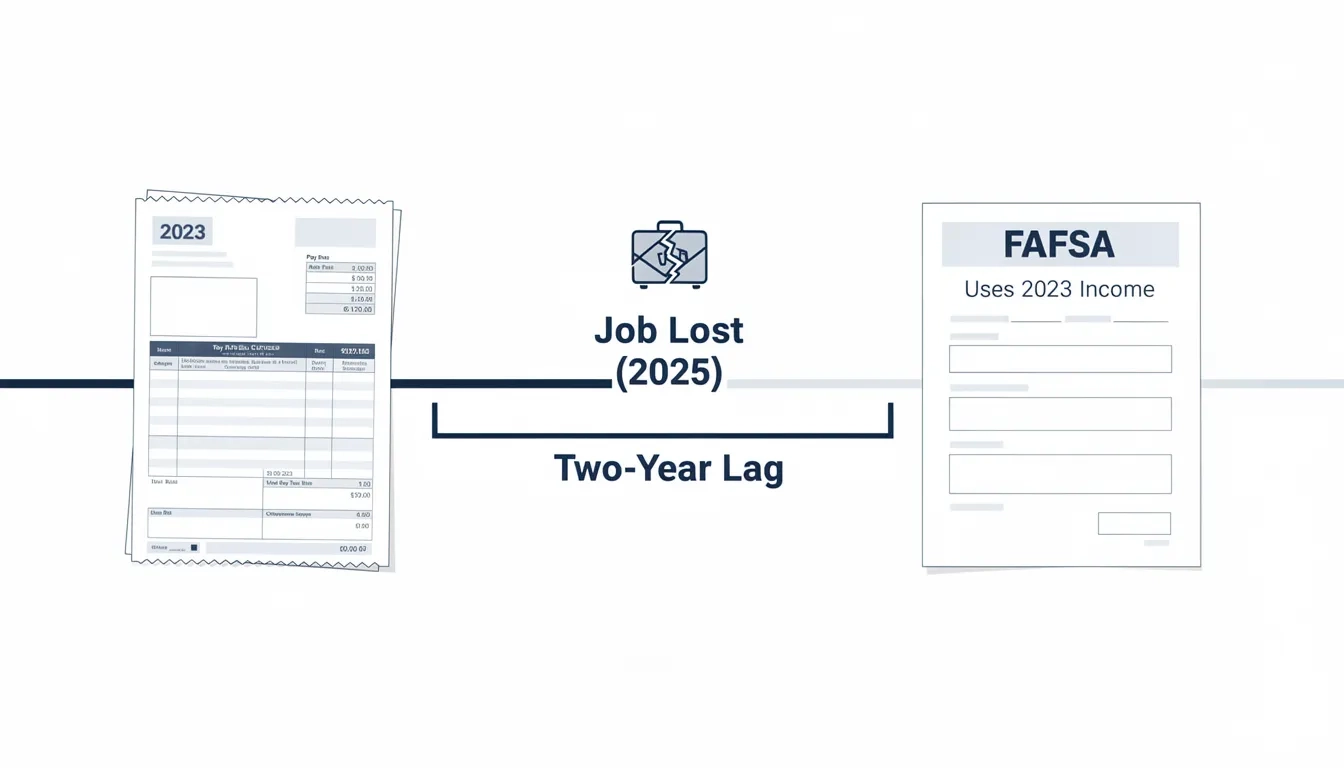

Your FAFSA doesn't know you lost your job. That's the uncomfortable truth, and it trips up thousands of families every year. The form relies on tax data from two years prior (the 2025-2026 FAFSA uses your 2023 returns, for instance), so a layoff that happened last month looks completely invisible to the formula. The numbers on file still show you fully employed.

This lag isn't a bug. The "prior-prior year" approach was designed so families could file earlier using already-completed tax returns, skipping the January scramble for W-2s. Sensible policy in stable times. But when a parent gets laid off or a student's income disappears overnight, the FAFSA reflects a financial picture that stopped being accurate the day the termination letter arrived.

If you don't act on it, nothing changes. The schools see the same old numbers. The aid stays the same.

Why the Student Aid Index Gets Stuck

The Student Aid Index (SAI) is the number that drives every need-based aid decision. Subtract it from a school's cost of attendance and you get your demonstrated financial need. A lower SAI means a larger gap, and a larger gap means more potential aid to fill it.

Income is weighted heavily in the formula. For dependent students, parent income above the income protection allowance gets assessed at up to 22% toward the SAI. Student income above $9,410 is assessed at 50 cents on the dollar. A high household income produces a high SAI. A high SAI effectively zeros out need-based eligibility.

When income drops sharply because of job loss and the SAI doesn't follow, families miss out on Pell Grants, subsidized Direct Loans, and institutional grants they'd otherwise qualify for. That's not an abstract bureaucratic problem. It's real money left on the table.

But the SAI only moves when someone triggers a recalculation. The FAFSA won't do it automatically.

Professional Judgment: The Legal Tool Most Families Don't Know About

This is where the conversation usually shifts for families who figure things out.

Professional judgment (PJ) is a provision in federal law that gives financial aid administrators (FAAs) explicit authority to adjust the data on your FAFSA when your circumstances warrant it. Chapter 5 of the 2025-2026 Federal Student Aid Handbook names job loss directly as a qualifying special circumstance. In documented unemployment cases, the FAA can project your current-year income as zero — a change that can dramatically lower your SAI and unlock aid you weren't previously offered.

The process is discretionary. FAAs have the power to help; they are not legally required to. Every case is reviewed individually, every school sets its own standards, and outcomes vary. Some aid offices move aggressively to help families in crisis. Others set high bars and review conservatively.

There are also firm legal limits on what FAAs can do. They cannot:

- Modify the SAI formula or its calculation tables

- Reduce reported income based on recurring household expenses like rent, utilities, or credit card payments

- Approve any adjustment without documenting specific reasoning in writing

- Apply their decision at any institution other than their own

That last point has real enrollment implications. An approval at one school stays at that school.

The Five-Step Process for Reporting a Job Loss

The sequence matters more than most families expect. A common mistake is contacting the financial aid office before filing a FAFSA — which creates confusion and delays everything. The system requires a FAFSA on file before an appeal can be reviewed.

Step 1 — Submit your FAFSA first. Use the prior-year tax data as required, even if it doesn't reflect the job loss. Get the form on file. You'll fix the discrepancy through the appeal.

Step 2 — Call or email the financial aid office within days. Not weeks. Explain the situation and ask about their special circumstances process. Most schools post an appeal form on their financial aid website. This conversation will tell you what they need and whether your situation qualifies under their criteria.

Step 3 — Gather your documentation. Standard packages typically include:

- A signed termination or layoff letter from the employer

- Pay stubs showing income in the final weeks of employment

- Unemployment benefit statements or a confirmation letter showing benefits were applied for

- Estimated total income for the current calendar year

- The most recently filed federal tax return

Step 4 — Submit everything at once. Incomplete packages sit in queue indefinitely. If mailing physical documents, use certified mail. Most schools now accept PDF uploads through a student portal.

Step 5 — Follow up one week later. Confirm receipt. Lost paperwork is the most common cause of delayed appeals, and offices don't always reach out proactively when something is missing.

What the Documentation Looks Like in a Real Case

Take a parent who worked in healthcare IT and was laid off in January 2026 after a round of corporate restructuring. Their 2023 W-2 showed $91,200 — exactly what the 2025-2026 FAFSA captured. Current income: zero from employment, plus roughly $23,847 annually from state unemployment benefits.

Their appeal package would include the layoff letter, final December pay stubs, the unemployment confirmation, and a written projection of their estimated 2026 income. The FAA now has documented grounds to recalculate using $23,847 rather than $91,200.

Depending on family assets and the school's cost of attendance, that shift could flip the student from no need-based eligibility to qualifying for a Pell Grant, convert unsubsidized loans to subsidized, and add institutional grant dollars that the original award letter never mentioned.

Job loss is the most commonly approved special circumstance in professional judgment reviews. Approval is never guaranteed — but your case starts with credibility rather than skepticism.

Timeline, Outcomes, and What to Do While You Wait

Speed matters more than most families anticipate. According to the University of Maryland's Office of Student Financial Aid, initial review takes 7-10 business days after a complete submission, with full decisions typically arriving 3-4 weeks after all required documents are received.

Here's how the stages typically unfold:

| Stage | Typical Timeline | Notes |

|---|---|---|

| Initial contact | Day 1 | Confirm eligibility; get the correct form |

| Document gathering | Days 2–7 | Layoff letter, pay stubs, unemployment confirmation |

| Complete submission | Day 7–10 | Send everything at once — partial packages cause delays |

| Initial review | 7–10 business days | Office confirms completeness |

| Full decision | 3–4 weeks total | FAA adjusts SAI if approved; student notified by email |

| Revised aid package | After approval | New award letter issued with updated aid |

One catch catches families off guard: your student bill is still due on the original date. The appeal review doesn't pause the billing cycle. Pay by the deadline, and if the appeal is approved, overpayments get refunded. Waiting out the review while delaying payment can generate late fees that don't reverse.

On outcomes: College Aid Pro's March 2025 research found that 75% of students at private colleges who appealed received additional aid, compared to 25% at public colleges. Typical increases ranged from $3,000 to $5,000 per year, with some exceeding $50,000. My read on that disparity: private schools have more institutional budget flexibility. They're more likely to have grant dollars available to reallocate. At a public university, the appeal is still worth filing — just go in with measured expectations.

If the appeal is denied, it usually means family assets (savings accounts, investments, home equity) keep the SAI too high for the income change to make a meaningful difference in need calculation. Frustrating. But useful information before you decide how much debt to take on.

When the Student Loses the Job, Not the Parent

Everything above applies to parent income changes. But the math shifts when the student is the one who got laid off.

Independent students — those who are 24 or older, married, veterans, or who support dependents — have their own income as the primary SAI input. A job loss here has direct and often dramatic effects on aid eligibility, sometimes more visible than a parent income change for a dependent student.

Dependent students who held part-time work face a different calculation. Losing a job that was paying $14,000 a year clears the $9,410 income assessment threshold and could modestly improve aid eligibility. The effect is real but smaller than a parent income change.

The professional judgment process works identically in both cases. Most schools maintain separate forms for dependent and independent students — ask for the right one during your initial contact with the financial aid office.

Bottom Line

A job loss won't automatically improve your financial aid. The FAFSA's two-year income lag makes recent hardship invisible until you take action.

- File your FAFSA first — appeals require a FAFSA on file, so don't delay submission waiting for the situation to stabilize

- Contact the financial aid office within days, not weeks; early contact gives the office time to work before billing deadlines close in

- Build your documentation now: layoff letter, recent pay stubs, unemployment confirmation, and a written estimate of projected annual income

- Pay your student bill on time while the appeal is pending — refunds follow approval, but late fees don't reverse

- File separately at every school you're considering — professional judgment decisions are institution-specific and don't transfer

The appeal process was designed precisely for situations like yours. Filing costs nothing except the time to gather documents.

Frequently Asked Questions

Does job loss automatically update my FAFSA and financial aid package?

No. The FAFSA captures income from two years prior, so recent job loss has zero automatic effect on your aid package. You have to proactively contact the financial aid office and file a formal special circumstances appeal before any administrator can adjust your Student Aid Index.

My FAFSA is already submitted with the higher income. Is it too late to appeal?

Not at all. Special circumstances appeals can be requested at any point during the academic year — before, during, or after your initial aid award is issued. A job loss that happens mid-semester can still trigger a review that affects the current term's aid. There's no hard deadline that permanently closes the window.

What's the biggest myth about FAFSA and job loss?

The most common mistake is self-disqualifying before filing. Families with substantial savings or home equity often assume their assets make an appeal pointless. But professional judgment reviews focus primarily on income changes, not asset totals. A significant income drop can meaningfully lower the SAI even when family assets haven't changed. File the appeal and let the administrator make the call.

How do I get my income recognized as zero if I'm currently unemployed?

The 2025-2026 Federal Student Aid Handbook allows financial aid administrators to set current-year income to zero when you provide unemployment benefit documentation or confirmation that you've applied for benefits. Submit supporting documents within 90 days of receiving them, though many schools accept older documents at the administrator's discretion.

Will filing an appeal affect my admission status or enrollment standing?

No. Financial aid offices and admissions offices operate independently. There is no mechanism — or incentive — to penalize students for requesting a special circumstances review. A denied appeal has no effect on enrollment status, academic standing, or future aid eligibility.

Can I file appeals at multiple schools simultaneously?

Yes, and you should if you're comparing enrollment offers after a major income change. Professional judgment decisions are institution-specific and don't carry across schools. Filing at each institution you're considering gives you comparable revised award packages — exactly the information you need to make a sound financial decision about where to enroll.

Sources

- Special Cases | 2025-2026 Federal Student Aid Handbook

- Special Circumstances Appeal Process | University of Maryland Office of Student Financial Aid

- Financial Aid Appeal: How And When To Ask For More Support | Affordable Colleges Online

- Can I Get a New Financial Aid Package if My Mom Lost Her Job? | Fastweb

- Reporting Special Financial Circumstances | Federal Student Aid

- How to Update FAFSA if Parent Loses Job | Earnest