Hidden College Costs Nobody Warns You About

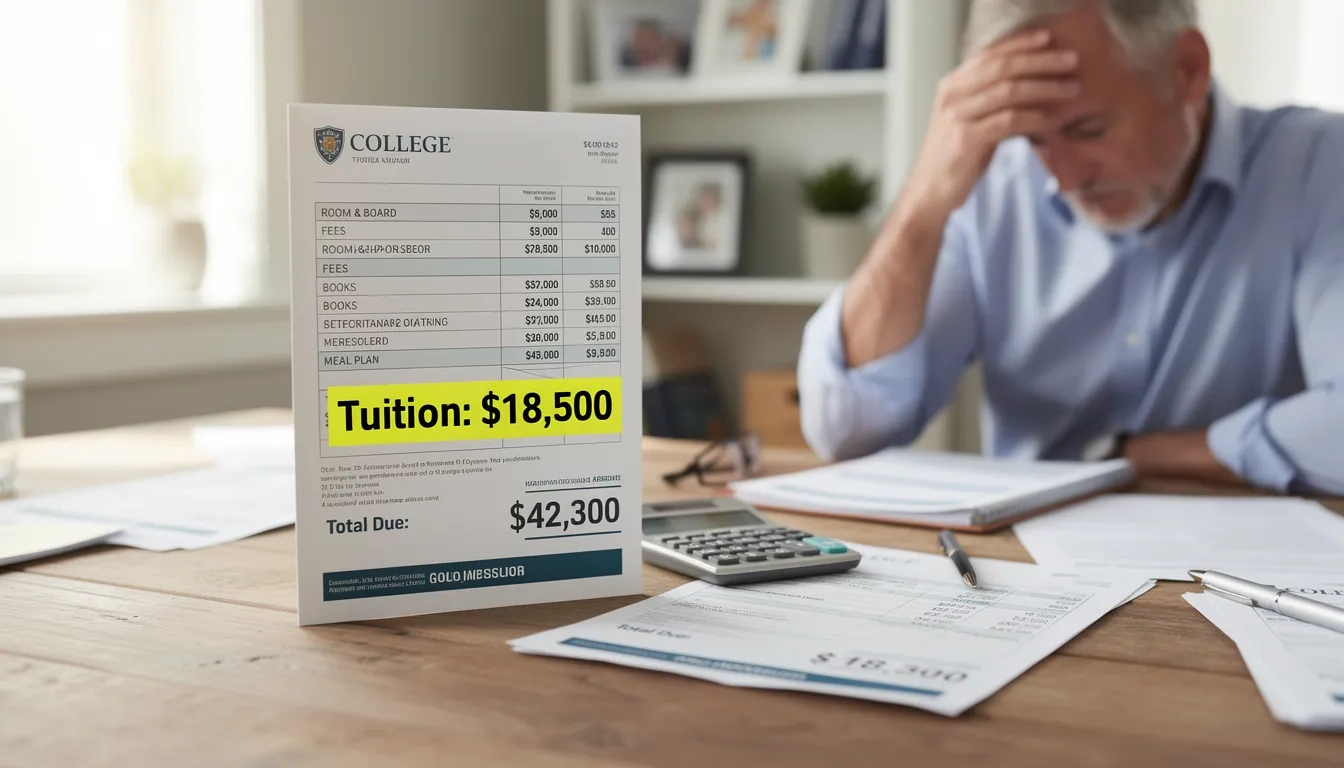

The University of Michigan lists its in-state tuition at $18,346 for the 2025–2026 academic year. The actual total cost of attending? Over $38,500. That $20,000 gap isn't buried in fine print. It's sitting in a document called the total cost of attendance, which most families never read and most students never fully understand.

The Number They Show You Isn't the Real Number

Colleges advertise tuition. Families budget for tuition. Then the first semester bill arrives and everything gets recalculated in a hurry.

A November 2025 report from Inside Higher Ed, funded by the Gates Foundation, found that only 27% of undergraduates fully understand their institution's cost of attendance. Nearly three out of four students are flying blind. Some face enrollment threats from an unexpected $100 bill (the report specifies one hundred dollars) because their actual financial picture was never explained clearly before they enrolled.

The total cost of attendance — not tuition — is the number that should anchor every college financial conversation.

| Type of School | Tuition & Fees Only | Total COA |

|---|---|---|

| Public 4-year (in-state) | $11,950 | $30,990 |

| Public 4-year (out-of-state) | ~$30,000+ | $50,920 |

| Private nonprofit 4-year | $45,000 | $65,470 |

Source: College Board, 2025–2026 academic year

At public schools, tuition makes up less than 36% of the total bill. The other 64% comes from expenses that rarely make the marketing materials — and that's exactly where families get surprised.

Mandatory Fees That Aren't Optional

Beyond tuition, most four-year colleges layer on a set of mandatory fees that appear at registration. Students cannot opt out. They're not prominently disclosed during the admissions process.

Technology fees are now standard at most institutions — typically $200 to $500 per year — covering campus Wi-Fi infrastructure, software licenses, and learning management systems. You pay these whether you ever set foot in a computer lab or not. Same with health service fees, student activity fees, and recreation fees.

Some schools charge an orientation fee for the mandatory orientation students must complete before classes start. Most charge a graduation fee when you finally finish.

Common mandatory fees students encounter each year:

- Technology/infrastructure fee: $200–$500

- Health services fee: $100–$350

- Student activity fee: $150–$400

- Athletics or recreation fee: $100–$300

- Orientation fee: $100–$200 (one-time, freshman year)

- Graduation/diploma fee: $50–$150 (one-time, senior year)

Together, these total $1,200 to $1,600 annually before a single textbook is purchased. If a school's website says "tuition: $12,000," the real floor for academic-year costs is closer to $13,500.

The Textbook Trap

Everyone jokes about expensive textbooks. Almost nobody actually budgets for them.

The College Board estimated full-time undergraduates spent an average of $1,240 on books and supplies in the 2021–22 academic year. Accounting for inflation since then, $1,400 to $1,500 is a more realistic planning number today. Some STEM students spend over $600 in a single semester.

Lab fees hit hardest in science, engineering, and art programs. A chemistry course may add $75–$150 per semester for consumable supplies. Architecture programs charge studio fees. Music programs charge lesson or instrument rental fees. These appear when you register for specific courses, not when you're browsing the catalog months earlier.

Then there's the access code problem. Publishers now routinely bundle textbooks with one-time-use online codes required to submit homework. Buying a used textbook without an unactivated code is largely useless — the code is how you're graded. A single course access code runs $80–$150, can't be shared or resold, and expires after one term.

Students who compare textbook prices across rental, used, and library reserve options during registration week — not the first day of class, when affordable copies are already gone — typically save $300–$500 per semester.

Room and Board's Quiet Takeover

If you're focused on tuition as the main cost driver, you're watching the wrong number.

At public four-year colleges, room and board now accounts for roughly 45% of total expenses, while tuition and fees make up less than 36%. That ratio has been shifting for years. Housing has become the dominant budget pressure in college finance, not academics.

On-campus room and board at public schools averages $9,000 to $12,000 per year. But that average conceals enormous variation. A school in a major metro area can charge $17,000 or more for on-campus housing. And here's what most families miss: mandatory meal plans are priced for maximum revenue, not actual student consumption.

A student who cooks occasionally might spend $180 per month on food if left to their own choices. A mandatory dining plan can cost $4,500 to $5,000 per year with minimal flexibility. Unused dining swipes at the end of a semester generally don't refund.

Off-campus housing sounds like the obvious fix. But it introduces costs students don't anticipate: utilities, renter's insurance, furniture, kitchen basics, and a security deposit often due before financial aid disbursements arrive. The savings aren't always what they look like from the outside.

The Semester-by-Semester Drain

This is the category that creates real financial trouble, because none of these costs feel large individually.

Transportation adds up fast. Parking permits at large public universities run $276 to $900+ per academic year depending on lot type and school. Students who commute add gas, insurance, and maintenance. Students without cars lean on rideshares — and $50 per month across nine months of school is $450 you didn't see in any COA estimate.

Student health insurance is a significant line item most families skip. A comparison of student health plans across 50 major U.S. universities found annual premiums ranging from $1,800 to $3,600 per year. Schools often require students to show proof of comparable coverage or auto-enroll in the school plan and charge the premium unless you actively waive it by a specific deadline — a deadline many students miss.

Personal expenses — laundry, toiletries, haircuts, clothes for internship interviews, phone bills — run $1,500 to $2,500 per year. College Board COA figures include a personal expense estimate, but families frequently skip past it assuming it's covered somewhere else. It isn't.

A realistic per-semester cost snapshot outside tuition, room, and board:

- Books and course materials: $700–$800

- Transportation and parking: $300–$500

- Personal expenses: $750–$1,250

- Health insurance (if not waived): $900–$1,800

- Social and extracurricular costs: $200–$1,000+

None of this appears in the tuition line.

Two Costs That Genuinely Catch People Off Guard

Scholarship taxation is one of the most widely misunderstood rules in college finance.

If a scholarship or grant exceeds a student's qualified education expenses — tuition, required fees, and required course materials — the excess is taxable income. Scholarship money applied to room and board, transportation, or personal expenses can generate a federal tax bill in April. A student receiving $25,000 in aid, with $12,000 covering tuition and fees and $13,000 going toward housing and food, could owe income tax on that $13,000. The IRS treats it like wages.

Most 18-year-olds don't know this. Neither do many of their parents. IRS Publication 970 covers the full rules, and a quick conversation with a tax professional early in freshman year prevents an ugly April surprise.

The second sleeper cost: changing your major. Switching programs mid-degree can add $15,000 or more to the total cost of a bachelor's degree. Required courses don't always transfer across departments. A pre-med student who pivots to psychology in junior year may need an extra semester — or a full year — to complete new distribution requirements. Students who fail or withdraw from a course pay full tuition, earn no credit, and must retake it at full price.

Nobody sells a college acceptance by saying "and if you change course in year two, budget an extra $15,000." But for the many students who do, that's real money.

My honest read: the way colleges communicate cost is structurally misleading. Tuition is the headline because it's the number schools can optimize for rankings. But tuition is not the number that determines whether a student finishes. The number that matters is the total cost of attendance, and only 27% of students actually understand it. This is not a financial literacy problem students need to solve alone — it's an information problem that schools should fix upfront, before enrollment deposits are paid.

How to Actually Budget Before You Commit

Start with the net price calculator, not the tuition page. Every federally-funded institution is required to publish one. It produces a personalized estimate based on family income and is far more useful than any sticker price.

Then add back what calculators routinely underestimate:

- Budget $1,400–$1,500 for books and materials, not the $500 figure some schools list

- Research whether the student health insurance plan is mandatory and look up the waiver deadline

- Find the actual parking permit cost if you're bringing a car

- Add a $1,000 emergency buffer per semester for unexpected expenses

- Verify whether dining plans are mandatory and calculate the real weekly cost

When comparing schools, compare net prices, not sticker prices. A private school offering $30,000 in aid on a $65,000 COA may cost a family less than a state school at $30,990 with no aid offer. The sticker price misdirects the comparison every time.

One more thing: aid packages can change after freshman year. Many merit scholarships carry GPA requirements, often 3.0 or higher. Some schools reduce award amounts for upperclassmen regardless of academic performance. Ask about renewal criteria before committing, and get the conditions in writing from the financial aid office.

Bottom Line

The number in the brochure is not the number you'll actually pay.

- Run the net price calculator at every school you're seriously considering — it takes 15 minutes and can expose thousands of dollars in planning errors

- Get the full COA, then add health insurance, parking, realistic book costs, and a $1,000 per semester emergency buffer before comparing offers

- Ask explicitly about aid renewal: what GPA is required, does the award scale down in later years, and is it guaranteed for all four years

- Talk to a tax professional early in freshman year if any scholarship money goes toward room, board, or personal expenses — the tax surprise is avoidable if you know it's coming

- Factor in a potential major change: if you're genuinely uncertain, estimate what one extra semester would cost before assuming a four-year finish

The full cost of college is knowable before you enroll. Most families just don't know which questions to ask.

Frequently Asked Questions

What is "total cost of attendance" and why does it differ so much from tuition?

Total cost of attendance (COA) is the full estimated annual expense of attending a school — including tuition, mandatory fees, room and board, books, transportation, and personal expenses. Schools publish these figures for financial aid purposes. The gap between tuition alone and total COA commonly runs $10,000 to $20,000 per year, and that gap is where most planning errors happen.

Are mandatory college fees ever waivable?

Rarely, and selectively. Student health insurance fees can sometimes be waived if you provide proof of comparable private coverage — but the waiver window is often short and easy to miss. Technology fees, activity fees, and recreation fees are almost never negotiable. Orientation and graduation fees are generally non-waivable. Budget for all of them.

Is the claim that textbooks cost over $1,000 per year really accurate?

Yes. The College Board's own data puts average annual book and supply costs at $1,240, and that figure doesn't fully capture one-time-use access codes that publishers now bundle with many course textbooks. Students in STEM, nursing, architecture, or art programs often spend significantly more. Renting textbooks, using library reserves, and buying prior editions when the professor permits can cut costs by 40–60%.

How does scholarship money become taxable income?

Scholarship funds used for tuition, required fees, and required course books are generally tax-free. Money used for room, board, transportation, or personal expenses is taxable — the IRS treats it like wages. You can't always avoid this if your scholarship exceeds your qualified expenses, but knowing about it before April prevents the surprise. IRS Publication 970 has the full breakdown in plain language.

How much can changing your major actually cost?

Depending on how far into a degree a student is when they switch, and how many credits carry over to the new program, a major change can add one semester to two full years of additional enrollment. At a public in-state school with a $30,990 total annual COA, one extra semester runs roughly $15,000. Students uncertain about their direction benefit from choosing programs with flexible general education requirements for the first two years.

Can a college reduce financial aid after freshman year?

Yes. Many merit scholarships carry GPA requirements, and some schools reduce aid amounts for upperclassmen regardless of academic performance. Some awards are one-year grants that don't renew at all. Always ask for the renewal criteria in writing before paying an enrollment deposit — a scholarship that makes year one affordable but doesn't guarantee years two through four is a different financial calculation entirely.